6 Things You Need to Know About Social Security Benefits

August 2017

If you are like most Americans approaching retirement, Social Security benefits will be a significant factor in maintaining a comfortable standard of living. So knowing your options and alternatives, plus the pros and cons of each, will be valuable as you consider the most beneficial approach for you in deciding what age is best for you to initiate Social Security payments based on your unique circumstances. That is the subject of this article.

The Basics

Full Retirement Age: Let’s start with when you may receive your maximum Social Security retirement benefits. That happens when you reach your “full retirement age”. For many years, it was age 65. However, as the average life expectancy of Americans has improved, that age increases gradually for people born in 1938 or later - finally becoming 67 for people born after 1959.

Again the significance of your full retirement age is that you then qualify for your full benefits under Social Security. Here’s a link to quickly determine your full retirement age.

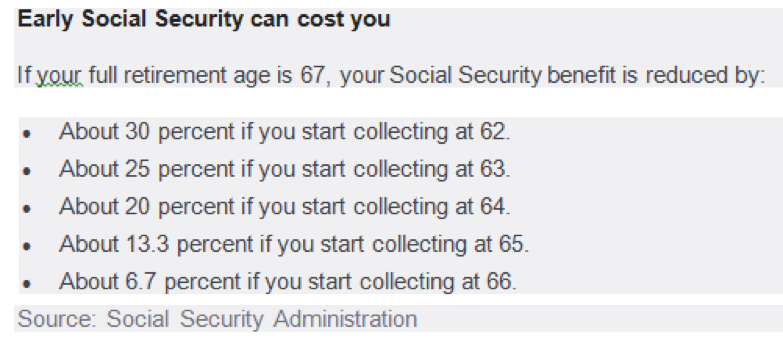

Earlier Retirement Age: At your option, you may choose to begin receiving Social Security retirement benefits as early as age 62 … albeit at a permanent significant reduction from income you would enjoy at your full retirement age. Here’s a look at what it could cost you.

You can estimate your benefits at various ages, including delaying your benefits beyond full retirement age to age 70.

Note: As stated by the Social Security Administration, "As a general rule, early or late retirement will give you about the same total Social Security benefits over your lifetime."

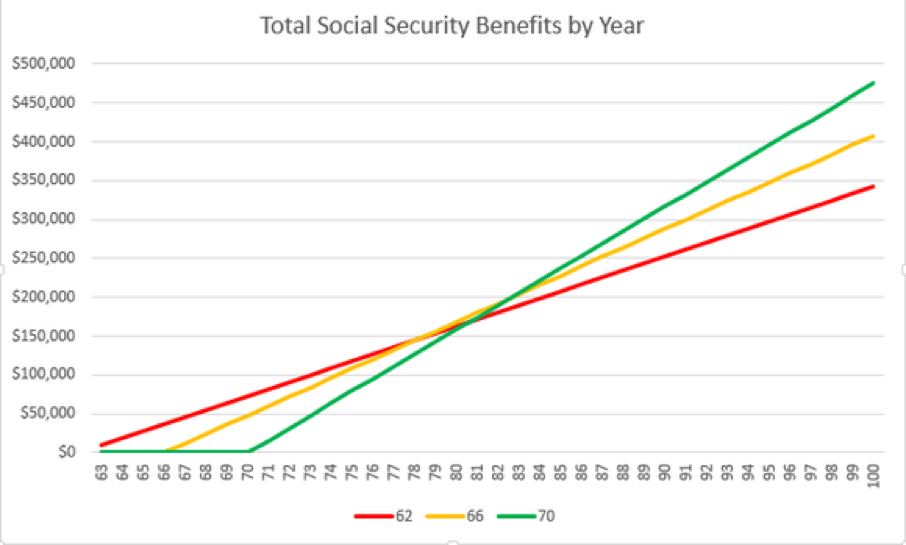

The chart below estimates the total amount of Social Security benefits received over a person’s lifetime depending on when they claim Social Security.

So back to the question of when to receive your first Social Security check. Certainly the choice is not one-size-fits-all. Postponing your benefits as long as possible to maximize your benefits may or may not be your best option. Consider your own financial needs, health and post-retirement plans before reaching your final conclusion of how to proceed.

There are six critical factors to weigh in determining your best course of action:

• Need for income

• Life expectancy

• Return on investment

• Post retirement employment

• Taxable withdrawals from retirement accounts

• Social Security as Taxable Income

Need for Income

This requires a very short commentary. If you absolutely need your Social Security benefits right now and you have at least reached age 62, you may choose to initiate your monthly income immediately.

Caution: If you continue to work while receiving Social Security, you may be subject to the government reclaiming some of your benefits if you exceed allowable earnings from your employment. That can be a shock if that demand occurs a year or more after you’ve begun receiving Social Security with a demand for immediate repayment. Be sure to seek guidance from your tax advisor to avoid any such surprises.

Life Expectancy

If you start collecting at the earliest opportunity, age 62, you’ll receive a permanently reduced benefit, but you could make out better overall if you live long enough to offset the reduction.

Refer to the above chart and note that if you claim at age 62, by age 78 you will have earned more in total benefits than if you began claiming at age 66. And only when you reach age 81 does claiming at age 70 net you more in lifetime benefits than claiming at age 62.

So if you’re anticipating a significant reduction in life expectancy, you might consider maximizing your lifetime Social Security benefits by claiming as early as possible.

Here’s a place to start your thought process. Of course, you will need to factor in elements such as current health, lifestyle, and family history that could increase or decrease life expectancy.

Return on Investment (ROI)

Earlier in this article, we looked at what Social Security can cost you in reduced benefits if you choose a retirement date sooner than your full retirement age. The flip side of that coin is what you stand to gain by delaying collecting benefits.

For each year that you delay collecting benefits, you will add 8% to your Social Security income. So now take a look at other funds you may have available to provide for your retirement – IRA, 401K and other investments. If you are not earning, and do not anticipate earning, at least 8% annually on these dollars, it is clearly in your best interests to push out receiving your first benefit check as long as possible by accessing these resources to provide income.

As an example, if you delayed your benefits until age 70, your monthly check will be 132% higher (4 years X 8%) than if you did so at age 66!

Likewise, if you like many Americans have “undersaved” for retirement, postponing your benefits as long as is practical will boost your future income from Social Security. That may mean working longer to lock in a bigger monthly check.

Another thought: If you choose to “retire early” and begin receiving your benefits before your full retirement age, remember that your Medicare health insurance doesn’t kick in until you are 65. So if you must pay for health insurance coverage, be sure to factor that additional expense as part of your decision-making.

Post-retirement Employment

If you choose to work after retirement, your earnings may negatively affect your Social Security benefits.

If you are under full retirement age for the entire year, the government deducts $1 from your benefit payment for every $2 you earn above the annual limit. For 2017, that limit is $16,920.

In the year you reach full retirement age, your benefit is reduced by $1 for every $3 you earn above $44,880 (in 2017) until the month you reach full retirement age.

You will also owe Social Security and Medicare tax on your earnings, even if you are already receiving benefits.

Taxable Withdrawals from Retirement Accounts

Every dollar withdrawn from a traditional IRA or 401K is taxed at ordinary income tax rates. When these withdrawals trigger the taxation of Social Security benefits, the taxpayer is pushed into a higher marginal rate. The calculation of this is somewhat complex and involves a topic called “provisional income”.

The details are beyond the scope of this article, so be sure to give us a call to discuss how your unique circumstances may be impacted.

And don’t think it best to be in the Post-retirement Employment section. It’s not just W-2 (earned) income that can create SSA to be taxable, but any income over a threshold. There are many who are fully retired and have their benefits taxed.

Social Security as Taxable Income

Taxation: Social Security benefits may be taxable income in the years received. The calculation and the defining circumstances are quite complex. Be sure to seek guidance from your tax advisor to determine how this may impact your tax situation.

Summary

OK. We think you agree that learning when and how to claim Social Security benefits is not child's play. It can be incredibly complicated depending on your financial needs, health and post-retirement plans. That said, time invested in getting the right benefit at the right time can make a big difference to your family's financial well-being.

No need to “go-it-alone”.

Give us a call to discuss best alternatives for your unique circumstances.